Well into the fifth year of Japan’s deregulated electricity retail market, which opened on April 1, 2016, there’s a lot to look back and reflect upon, and there’s still much to be anticipated.

We’re going to zero in on some interesting aspects of the winding road the market has taken so far.

Hiccups, Haze and Uncertainty

As has been the case in many countries, not everything went smoothly when the market opened in Japan.

Out the gate, TEPCO ran into problems transmitting customer usage data to retailers serving load in the TEPCO Power Grid zone, and a number of retailers were unable to bill their customers for several months as a result. The customer switching system has been rife with problems too, and even three or four years into the market many retailers were seeing switch rejection rates in the range of 10%, leading to bloated staffing costs.

At the end of 2018, the Ministry of Economy, Trade and Industry (METI) announced that more than 20% of electricity customers had switched their power provider, but it turns out that nearly 40% of those switches were by customers who simply switched from their old regulated tariffs to new deregulated rate plans at the same incumbent power companies they had been with prior to deregulation.

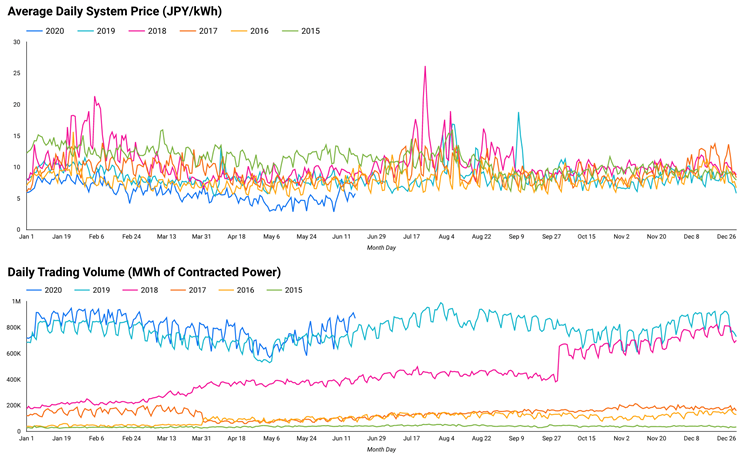

When the market opened, only about 3% of power being delivered nationwide was traded on the Japan Electric Power Exchange (JEPX). There was great anticipation that once enough nuclear plants had been restarted from their post-Fukushima shutdowns to provide around 15% of nationwide generation, the government would require the utilities to sell a substantial portion of that restored baseload power on JEPX in order to boost wholesale market liquidity. Only a small fraction of the nuclear plants have come back online to date, never exceeding about 5% of generation and recently coming back down slightly, but nonetheless, the wholesale market has grown drastically more liquid, with as much as 31% of power delivered being traded on JEPX. Contracted volumes on JEPX have gone from being relatively flat before deregulation to clearly reflecting demand patterns, and there has been a downward trend in average wholesale prices except around some extreme weather events.

Source: JEPX. Interactive chart at: shulman-advisory.com/jepx.

Even as the wholesale market – which is where non-generating retailers currently source about 70% of their power – got livelier, however, there were still bumps in the road. In mid-2017, a number of retailers got their wrists slapped by the Electricity and Gas Market Surveillance Commission for submitting supply plans to the Organization for Cross-Regional Coordination of Transmission Operators (OCCTO, the national grid coordination organization, which has a mandate that doesn’t quite correspond with that of an ISO, TSO, or other organizations commonly found in other markets) in which they had not scheduled any power for delivery. The reason was that for a time, real-time clearing prices were consistently lower than the day-ahead prices available on JEPX. METI sent the “offending” companies letters telling them to cut it out.

Another important development in 2017 was an increase in the stringency of the Surveillance Commission’s reviews of retailer license applications. As the number of licensed retailers climbed towards 450, METI decided that it had issued too many licenses to companies which had not been properly equipped to get their businesses off the ground, and even companies which had not started selling power after receiving their licenses. As a result, license review times, which had gotten as short as three months even for some foreign entrants into the market, started stretching close to a year for many applicants. METI’s best intentions had the ironic effect of causing a number of companies which may well have been able to launch successful businesses to burn so much cash while waiting for their licenses to be issued that they no longer had the resources to properly grow their businesses once they were licensed.

As of today, the majority of the half dozen or so American retailers which have entered the market have sold their assets to other entities and essentially pulled out of the market. There are more than 150 licensed retailers which have not served any customer load – out of a list of licensed retailers which recently broke the 700 mark – and METI stated in late 2019 that it’s going to start revoking licenses not only from bad actors in the market, but also from companies who are sitting on licenses for no apparent reason.

If this all indicates that we’re now in one of the cycles of contraction which commonly occurs three or four years after a new market opens, there are also signs that we may well enter a new cycle of growth and opportunity soon.

Stay tuned.